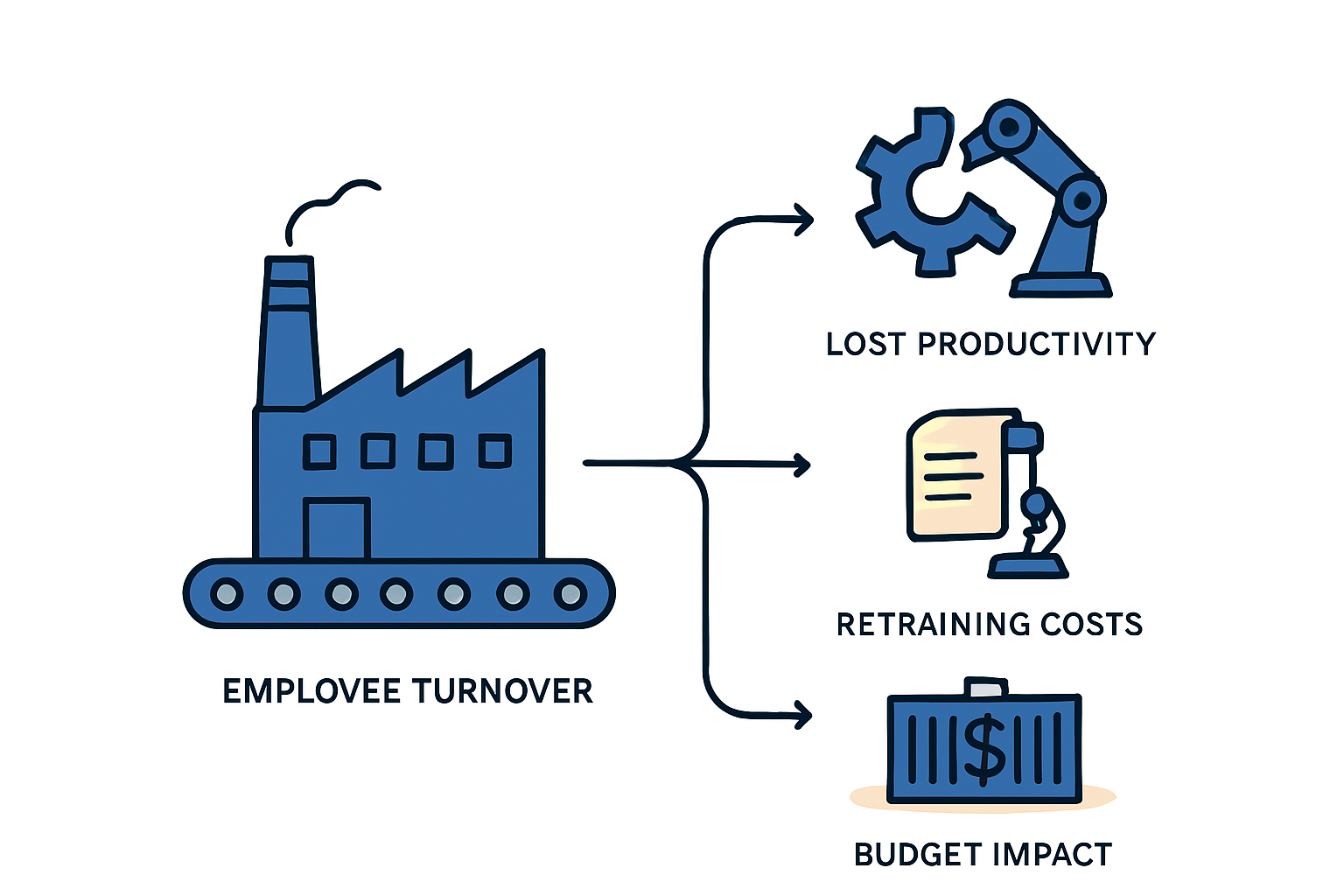

Budgeting for Reality: Modeling Employee Turnover Costs in Your Factory’s Financial Plan

A familiar scenario unfolds in many new industrial ventures. An entrepreneur develops a meticulous multi-year business plan, accounting for machinery, materials, and salaries. The factory launches, operations begin, and for the first year, everything seems to align with financial projections. By year three, however, a problem emerges: labor costs are consistently 15-20% over budget, even though headcount hasn’t increased. The source of this financial leakage is often an unbudgeted, yet entirely predictable, operational expense: employee turnover.

Failing to account for the recurring costs of replacing and retraining staff is one of the most common oversights in operational budgeting. This article provides a clear methodology for calculating and integrating these costs into a long-term financial plan, transforming them from a reactive crisis into a manageable, forecasted expense.

The Unseen Expense in Manufacturing Operations

Employee turnover is more than just the cost of a replacement salary. It encompasses a cascade of direct and indirect expenses that impact productivity and profitability. Industry research offers a reliable framework for understanding this financial impact.

A comprehensive 2022 report by the Society for Human Resource Management (SHRM) found that the total cost to replace an employee is, on average, six to nine months of that person’s annual salary. For a specialized technician or operator in a manufacturing facility, the financial impact is substantial. An employee earning $60,000 per year could cost between $30,000 and $45,000 to replace. Multiplied across an entire workforce, these costs can significantly alter a company’s financial health.

These costs fall into two main categories:

- Direct Costs: These are the easily quantifiable expenses associated with the hiring process, including fees for job advertisements, recruitment agency commissions, pre-employment screening, and the administrative costs of onboarding a new hire.

- Indirect Costs: These are less tangible but often more significant. They include the value of lost production while a position is vacant, the reduced output of a new employee during their learning period, and the time senior staff must divert from their core duties to train the replacement.

For a business owner, viewing labor costs as a static line item in the operational budget is a critical planning error. A resilient financial model treats turnover as a recurring, predictable cost of doing business.

Understanding the Four Phases of Turnover Cost

The cost of replacing an employee isn’t a one-time event. It’s spread across a cycle of events, each with its own costs. Understanding this cycle is the first step toward accurately modeling its financial impact.

Phase 1: Separation Costs

The first costs are incurred the moment an employee leaves. This includes administrative tasks related to processing the departure, conducting exit interviews to gather feedback, and paying out any final salary or accrued benefits. In some cases, it may also involve the cost of temporary staff to cover critical duties until a replacement can be found.

Phase 2: Vacancy Costs

This phase represents the productivity lost while a position is vacant. Deadlines may be missed, production targets might be lowered, and remaining team members may have to work overtime to compensate, leading to burnout and increased payroll expenses. This is a period of pure loss, where the salary for the position is saved, but none of the work’s value is being generated.

Phase 3: Recruitment Costs

This is the most visible phase, involving all the activities required to find and hire a new employee. Costs include:

- Advertising the position on job boards or with industry publications.

- Time spent by management and HR personnel reviewing applications and conducting interviews.

- Background checks and skills assessments.

- Potential recruitment agency fees, which can be a significant percentage of the new hire’s first-year salary.

Phase 4: Training and Onboarding Costs

Once a candidate is hired, a final and often prolonged phase of costs begins. According to a study by Training Industry Quarterly, it can take a new employee in a complex technical role up to two years to reach the full productivity of an experienced predecessor. During this “productivity gap,” the company is paying a full salary for reduced output.

This phase also includes the direct costs of formal training programs and the indirect cost of time that supervisors and experienced peers must dedicate to mentoring the new hire, diverting them from their own productive tasks.

How to Calculate a Realistic Turnover Provision

A prudent business plan anticipates turnover instead of just reacting to it. This means creating a “turnover provision” within the annual budget—a straightforward calculation based on three key variables.

Step 1: Estimate Your Annual Attrition Rate

The attrition rate is the percentage of your workforce you expect to leave in a given year. While precise figures vary, industry data provides a solid baseline. For instance, the U.S. Bureau of Labor Statistics reported high separation rates in the manufacturing sector. In many emerging markets, turnover for skilled labor is commonly estimated to be between 15% and 25% annually. For a new factory, it’s wise to start with a conservative estimate, such as 20%.

Step 2: Calculate the Average Cost Per Replacement

Using the SHRM guideline of 6-9 months of salary provides a reliable starting point. A median figure of 7.5 months is a balanced choice for financial modeling.

- Formula: Average Cost Per Replacement = (Average Annual Employee Salary / 12) * 7.5

Step 3: Build the Annual Turnover Provision

With these figures, you can calculate the total amount to set aside in your operational budget.

- Formula: Annual Turnover Provision = (Total Number of Employees) (Estimated Attrition Rate) (Average Cost Per Replacement)

Example Calculation:

Consider a new solar module factory with 50 production employees and an average annual salary of $30,000.

- Estimated Attrition Rate: 20%

- Average Cost Per Replacement: ($30,000 / 12) * 7.5 = $18,750

- Number of Expected Departures: 50 employees * 20% = 10 employees

- Annual Turnover Provision: 10 employees * $18,750 = $187,500

This $187,500 is the amount the business should budget annually to cover the predictable costs of employee turnover. It can be broken down into monthly or quarterly allocations.

The Strategic Impact Beyond the Balance Sheet

The consequences of high turnover extend beyond direct financial costs. Research from the Journal of Operations Management demonstrates a direct link between high staff turnover and increased product defect rates. New employees, still navigating the learning curve, are more prone to procedural errors, which can compromise quality and lead to waste or rework.

Furthermore, high turnover can erode institutional knowledge—the unique, experience-based understanding of processes and equipment that isn’t written down in any manual. When veteran employees leave, they take this valuable knowledge with them, and it can take years for the organization to recover it.

Mitigating Costs Through Proactive Strategy

While budgeting for turnover is a necessary defensive measure, the most effective long-term strategy is to reduce it. Investment in retention is almost always more cost-effective than financing attrition.

One of the most powerful tools for retention is investment in employee development. According to the Association for Talent Development (ATD), companies that offer comprehensive training programs report significantly higher performance metrics. Such programs not only create a more skilled and productive workforce but also signal to employees that the company is invested in their long-term career growth, fostering loyalty.

Based on experience from J.v.G. turnkey projects, establishing clear career progression paths and a supportive management culture from day one is critical, especially in a new factory environment. These foundational elements help ensure that the initial team remains stable as the operation matures.

Frequently Asked Questions About Workforce Budgeting

How does turnover in a new factory differ from an established one?

Turnover can be higher in the first 1-2 years of a new factory’s operation. This period often involves resolving initial cultural fit issues and refining roles. New ventures are wise to budget for a slightly higher attrition rate at the outset.

Are these cost ratios applicable in regions with lower labor costs?

Yes. While the absolute dollar amounts will be lower, the ratio of replacement cost to annual salary (e.g., the 6-9 month rule) tends to hold true across different economies. The loss of productivity and the costs of recruitment and training are universally proportional to the local salary structure.

Can good management significantly reduce these costs?

Absolutely. Management quality is the single most important factor in employee retention. A well-managed, respectful, and organized work environment directly reduces voluntary turnover, delivering a substantial return on investment through lower replacement costs.

What is a “healthy” turnover rate?

This varies by industry and region. In manufacturing, an annual rate below 10% is generally considered very strong. A rate between 10% and 15% is often seen as manageable. Rates consistently above 20% typically indicate underlying issues in management, compensation, or work environment that require strategic attention.

Acknowledging employee turnover as a standard operational variable and embedding it in the financial planning process helps a business owner build a more resilient, predictable, and ultimately more profitable enterprise. It is a fundamental shift from hoping for stability to planning for reality.